President’s Toronto SUN Column: Condo Living An Affordable Alternative

Author: Toronto Real Estate Admin / Category: Toronto RealtorTREB President’s Column as it appears every Friday in the Toronto Sun’s Resale Homes and Condos section.

September 19, 2014 — If there were ever a city aware of the dangers of falling victim to its own success, it’s Toronto, where on any given day you’re likely to encounter a water cooler discussion about house prices.

Millions of people share a love of the Greater Toronto Area and together we have built an amazing city that routinely receives top marks in global rankings. This year alone, our city has earned the titles of world’s most tax-competitive, intelligent, resilient, and youthful in various independent studies. Most recently, we were named the world’s fourth most livable city in a ranking by the Economic Intelligence Unit, a British research and analysis firm.

As a result of our city’s popularity though, the cost of owning a home in the GTA has grown exponentially in recent years. In July, the average price of a GTA home was $550,700. Compare that to the average price of $395,414 five years ago and the result is a 39 per cent increase.

Despite these staggering numbers, there’s no reason to be discouraged if you haven’t yet taken the plunge into the housing market. Condominium living offers affordable alternative to low-rise housing that boasts the convenience of a maintenance-free lifestyle with proximity to countless business opportunities and entertainment options.

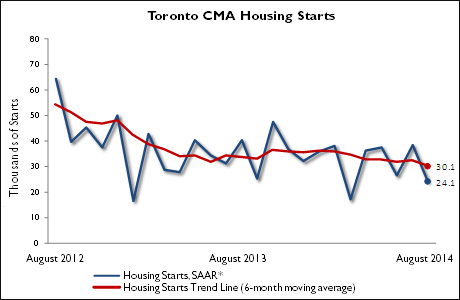

As evidence of its popularity, you need only to look to the skies: downtown Toronto is a veritable fairground of cranes putting together the latest enticing approach to urban living. In fact, there are now more high-rise buildings under construction in Toronto than anywhere else in North America. Currently 130 developments are underway here compared to 91 in New York City.

When you compare the average cost of a detached home to that of a condominium apartment it’s no wonder so many people have embraced the condo lifestyle. In July, an average detached GTA home would cost you $695,745 whereas an average condominium apartment would run you $357,345.

Based on a five-year fixed rate mortgage with 4.79 per cent interest amortized over 25 years, these costs represent the difference of a monthly mortgage payment of $3,963.72 for a detached home compared to $2,035.82 for a condominium apartment.

Canada Mortgage and Housing Corporation recently released the results of its 2013 Condominium Owners Survey and the findings illustrate just how much we have come to embrace this housing type. The survey found that more than 58 per cent of investors living in the Greater Toronto and Vancouver Areas plan to keep their last purchased condominium unit for more than five years, which shows confidence in the market’s long-term outlook.

If you’re considering the purchase of a condominium apartment either as an investment or a first home, I encourage you to talk to a Greater Toronto REALTOR®. In addition to searching resale offerings in the Multiple Listing Service®, they can access a database of new home developments throughout the GTA and provide you with information on government programs to put your goals within reach.

Be sure to visit www.TorontoRealEstateBoard.com as well, where you’ll find updates on the market, open house listings, neighbourhood profiles and much more.

Paul Etherington is President of the Toronto Real Estate Board, a professional association that represents 39,000 REALTORS® in the Greater Toronto Area.

Follow TREB on www.twitter.com/TREBhome, www.Facebook.com/TorontoRealEstateBoard and www.youtube.com/TREBChannel

Article source: http://www.torontorealestateboard.com/market_news/president_columns/pres_sun_col/index.htm