TREB & BILD Stress That Demand for Home Ownership Remains Strong

Author: Toronto Real Estate Admin / Category: Toronto RealtorTORONTO, November 25, 2014 — Greater Toronto, November 25, 2015 – Demand for home ownership remains strong in the GTA, and dynamics around housing supply are impacting prices and redefining the market, said the Building Industry and Land Development Association (BILD) and the Toronto Real Estate Board (TREB) at their first ever joint briefing on the state of the GTA housing market.

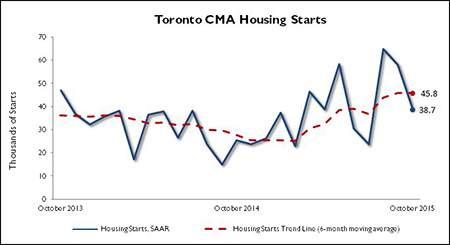

Through the first 10 months of 2015, there were 124,123 new and resale homes sold in the GTA. A record number of sales were reported through TREB’s MLS(R) system. New home sales reported by RealNet Canada Inc. (an Altus Group Company) were consistent with the 10-year average, but the mix and type of new homes being sold as well as their prices have changed.

Total new home inventory levels have remained within the normal range at 26,388 homes, but more than 81 per cent of those homes are high-rise condominiums, according to RealNet Canada Inc. (an Altus Group Company).

Builder inventory of new low-rise homes, including detached, semi-detached and townhomes, was at 4,980 homes at the end of October, a near record low. As of October 31, there were 10,014 low-rise properties available for sale on TREB’s MLS(R) system. There were 16,079 new and 12,773 existing low-rise homes available for sale at the end of October 2005. While the supply of low-rise homes has trended lower over the last decade, demand has remained strong, pointing to more competition between buyers and very strong price growth.

The average price of a new low-rise home as of October 31, 2015 was $802,376 – more than double the average price in 2005, which was $387,369.

A similar trend has been noted for TREB MLS(R) transactions. The MLS(R) HPI Single-Family Benchmark Price increased to $669,400 in October 2015 from $363,100 in October 2005.

The new high-rise market saw an increase in supply in the last 10 years. There were 21,408 new high-rise homes available for sale across the GTA at the end of October 2015 compared to 13,006 a decade ago. The average price of a new high-rise unit was $440,382, up from $288,587 in 2005.

Price growth for TREB MLS(R) transactions was similar over the same time period with the MLS(R) HPI Apartment Benchmark Price in October at $331,400 compared to $207,800 in October 2005. It is important to note that while we have seen strong new condominium apartment completions and subsequent new listings on TREB’s MLS(R) system, these newly listed units have been largely absorbed. Far from seeing a glut in supply, the months of inventory trend has declined and growth in the MLS(R) HPI Apartment Benchmark Price has accelerated compared to last year.

The size of new condominiums brought to market has decreased over the last 10 years. The average new high-rise home in October 2015 was 767 square feet, compared to 908 square feet in 2005.

“As an industry we continue to find innovative ways to provide a range of housing choices,” said BILD Chair Steve Deveaux, vice-president of Tribute Communities. “But it is becoming increasingly challenging to design, build and sell the homes that many people – especially first-time buyers – want to and can afford to purchase.

For new homes, single-detached homes saw the largest year-over-year price increase in October. The average price of a new detached home in the GTA was $962,312.

“To comfortably afford that home with a 20 per cent down payment, the buyer would need an annual income of $174,854,” Deveaux said. “With a smaller down payment, the required income would be even high

er. According to Statistics Canada, the average total family income in the Toronto area in 2013 was $107,200.”

The development industry is building more condominiums than it did a decade ago, but as the GTA continues to grow by up to 100,000 people every year, demand for low-rise homes has not decreased.

Deveaux said that demand for detached, semi-detached and townhomes is outpacing supply, which is limited due to a lack of serviced land designated for development.

TREB president Mark McLean said the industry is concerned about the disconnect between some current government policy initiatives and homeownership affordability. TREB cites the Ontario government’s plan to allow municipalities to charge their own municipal land transfer tax as the most recent example.

“Homebuyers in the GTA presently benefit from a diversity of new and existing home options that are affordable at different income levels,” McLean said. “Sadly, the provincial government seems bent on hampering home ownership affordability. Studies have shown that municipal land transfer taxes will have a negative impact across Ontario, not only from an affordability perspective, but also by undermining our economy and costing thousands of jobs.”

Government fees and taxes amount to an average of one-fifth the cost of a new home in the GTA, according to a BILD-commissioned study in 2013. This drives up the cost of new homes and later trickles down to the resale market.

The organizations stated that it’s important for governments to educate residents about the effects public policy changes will have on the state of the housing market in the GTA.

“This industry is extremely important to the economic growth and prosperity of our cities and it’s important for GTA residents to understand what drives and impacts it,” Deveaux said.

About BILD

With more than 1,450 members, BILD, formed through the merger of the Greater Toronto Home Builders’ Association and Urban Development Institute/Ontario, is the voice of the land development, home building and professional renovation industry in the Greater Toronto Area. BILD is proudly affiliated with the Ontario and Canadian Home Builders’ Associations. www.bildgta.ca

About TREB

Greater Toronto REALTORS® are passionate about their work. They are governed by a strict Code of Ethics and share a state-of-the-art Multiple Listing Service. Over 42,000 residential and commercial TREB Members serve consumers in the Greater Toronto Area. TREB is Canada’s largest real estate board.

www.TREBHome.com

For additional statistical information or to set up an interview, contact Andrei Zaretski or Amy Lazar.

Mary Galagher

Senior Manager,

Toronto Real Estate Board

416-443-8158 or 416-419-8133

mary@trebnet.com

Andrei Zaretski

Public Affairs Manager, Marketing Media Relations

Building Industry and Land Development Association

416-391-3450 or 416-843-4898

azaretski@bildgta.ca

Article source: http://www.trebhome.com/market_news/release_market_updates/news2015/nr_bild_ownership_demand_112515.htm